It’s been said that buying a home is one of life’s bigger decisions, but selling isn’t something to be taken lightly either—especially not in Toronto, among the country’s most competitive and real estate markets and by far its most active.

In 2018, more than 77,000 homes changed hands, according to the Toronto Real Estate Board (TREB), and that was a double-digit decrease from the previous year (and that total doesn’t even include pre-construction purchases). Whether upgrading to a bigger house for a growing family or downsizing to a condo during retirement, all the steps towards selling a Toronto home may be overwhelming. So Justo has put together the ultimate guide to selling a home in Toronto to walk you through every step along the way.

Related article: I’m Selling My House. What Do I Need to Know?

1. Select a realtor

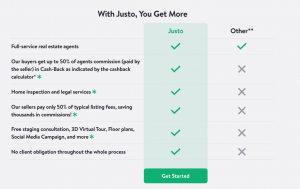

With so much at stake, you’re going to want the help of professionals. TREB claims more than 50,000 members across the GTA, so it’s going to be important to do your research. Justo’s rock-bottom seller’s commission of 1.25%—that’s about half the usual rate—and roster of experienced professionals, from real estate lawyers to home stagers, can save you valuable time.

Read testimonials. Ask friends and family who have recently sold their homes for their experiences and recommendations. You should also check out realtor social media channels — such as Twitter, Facebook, and Instagram (if they don’t have an online presence beyond a website, they may not have the best handle on digital marketing, which is important and will come up later). Not only that, but you might discover personal views or values that aren’t in line with your own or may offend possible homebuyers down the road. It’s always best to check.

2. Read your listing agreement carefully

So you’ve found your realtor. Time to sign on the dotted line, as you’re entering into a contract with a brokerage. Don’t just skim the paperwork. Make sure you understand everything and don’t be afraid to negotiate. If you’re not sure about something, ask!

In fact, questions can help you decide whether or not you’ve found the right realtor for you. Here are some questions to ask:

- “How much experience do you have in the Toronto market?”

- “What do you plan to do to market my home?”

- “What sets you apart from other realtors?”

- “How would you describe your negotiation style?”

- “Will I be dealing directly with you at all times?”

- And, perhaps most importantly, “Can I see some references?”

3. Now, hire a real estate lawyer

Like when you hired your realtor, you’re going to want to vet a lawyer carefully. Your realtor should have a referral. When working with a full-service brokerage like Justo, you won’t have to worry about spending valuable time making phone calls and sending emails looking for legal help. Whatever the case, it’s ideal to have your lawyer hired early in the process because you’re going to be busier in the steps that follow.

4. Prepare your home for listing

Most homes are going to need some TLC before they’re ready to hit the market, and you may want some help. Fortunately, there are professionals who are trained in this very aspect of the home-selling process.

Consider a professional stager

A home stager can make life a lot easier, since they’ll arrange it all: renting stylish furniture and storage space for your own stuff, touching up rooms, de-cluttering.

You can expect to pay between $1,500 all the way up to $10,000 (for a large estate) to hire your own home stager. If that sounds like a lot, remember that according to one study by the Real Estate Staging Association (RESA), 68 percent of staged homes sold for 9 percent more than neighbouring homes that weren’t professionally staged. For perspective, the average price of a GTA home was $820,148 this April, according to TREB, and 9 percent of that is nearly $74,000.

Another way to show the value of home staging also comes from the association. Homes that are staged before listing sell 90 percent faster than homes that are listed unstaged and then staged afterwards, according to a RESA infographic. As per the findings from a study of 1,081 homes, those that were staged before appearing on the online-listing system spent 23 days on market, versus 225 days for properties that were initially unstaged.

Browse websites of stagers in the city. Some will have Pinterest pages, and that should give a sense of their work and inspiration. Learn as much as you can about their style and then book a consultation. This will give you a chance to see if you work well together, which is important because you’ll be entrusting them with your home. Don’t wait for the last minute, because in-demand stagers will require advance bookings.

Or do it yourself — but do something

A stager isn’t in your budget? You should at least repaint your home (neutral colours are best) buy and install new light bulbs to make the place really shine, rent a carpet steamer, ensure the place is tidy, take out oversized furniture, and try to remove particularly personal touches. Family portraits, your dog’s favourite bed, and kids’ paintings hanging on the fridge don’t help. After all, you want potential buyers to be able to picture themselves living in your home. Don’t neglect your garage, unfinished basement or crawlspace. These parts of your home might not ever glow, but you can highlight storage potential by clearing them out.

Flip through magazines like Style at Home and Designlines (or visit their websites) to get a sense of current trends and try to make the time to visit open houses in the area so you can see what they’ve done and size up how your home compares.

Related article: Toronto online platform touts its buyer/seller experience

5. Decide when you’d like to list

Everybody’s circumstances are unique, but it literally pays to put some thought into exactly when to list a home for sale in Toronto. Seasonal factors, which are described below, are an important consideration.

However, increasingly government policies have been impacting home sales, from mortgage rules to new taxes. Whenever new policies are introduced by a level of government, many would-be homebuyers step to the sidelines and take a wait-and-see approach. That was certainly the case when the Ontario government introduced the Fair Housing Plan, which included a foreign-homebuyer tax for Toronto and the broader Greater Golden Horseshoe region. Conversely, homebuyers were highly motivated towards the end of 2017 because federal policymakers had announced that lending rules were going to be tighter starting January 2018 with a new mortgage stress test. Afraid that they wouldn’t be able to qualify for a mortgage once the test came into effect, some homebuyers rushed to buy before the year’s end.

New policies notwithstanding, typically, May and June are the two months that see the most home sales in Canadian markets. But one recent study found that homes in Toronto proper that sold between late April and early May actually landed the highest premium, an extra $33,000, in fact, so it can be worth it to list a little earlier in the spring.

However, the study notes there are positives to selling at times other than spring.

Summer

Homes do look great in the bright summer light, and it can really showcase certain features, like a house’s big windows or a backyard deck and pool. Same goes for condo balconies and terraces, or shared open-air amenities like a rooftop pool.

Fall

In autumn, buyers—at least those with kids—likely want to hurry up and close before the school year gets too hectic and schedules are tighter, so a Toronto home seller can get an edge then.

Winter

Similarly, anyone looking for a home in the winter and over the holidays is likely eager to make an offer, just remember you’ll be dealing with a limited pool of buyers. Harsh winter months, like February 2019, have been known to seriously hinder home sales.

6. Complete a pre-list home inspection

Homebuyers will want to do their due diligence and have a home inspection done. However, before listing a home, the current owners should have their own inspection done to identify any potential problems, so they can be reflected in the future asking price. New windows can be a selling point, whereas a leaky roof—not so much. Then the decision can be made whether to fix any issues or list the home as-is. Trying to save a little money by foregoing this step is not worth it.

7. Put all your paperwork in order

You’ve probably realized by now that selling a home in Toronto comes with lots of paperwork. Here’s a rundown of what to pull together:

- You’ll need copies of your latest hydro, heating and tax bills.

- Track down any relevant manuals, such as for an air conditioner, furnace, or, if you’re leaving them behind, appliances.

- Dig up the survey, which outlines info from a property’s natural features, such as trees, to structural elements.

- If selling a condo, a condo status certificate is required. The document, unique to condo/strata ownership, details the condo corporation’s financial status, including how much money is in reserve and the budget, as well as minutes from the latest annual general meeting.

- You should create a document outlining every reno and repair done since you purchased the property (as well as the accompanying bills). Highlight any issues uncovered during the pre-list inspection, as you’ll want to be honest and open about these so you avoid potential legal issues down the road.

(At this point, don’t forget to get keys cut, so your realtor can easily show your home using a lockbox.)

8. Name your price

Deciding how much to list your home for depends on a variety of factors, including current market trends, location, features, possible issues identified through your pre-list inspection, and more.

Here’s a rundown of some major factors that will influence what buyers are going to be willing to pay:

The state of the market

Is it a buyer’s market, a balanced market, or a seller’s market? One way to quickly gauge this is by checking out the local sales-to-new listings ratio. A ratio between 40 to 60 percent generally reflects balance, while anything below is a buyer’s market and anything above is a seller’s market. Basically, a ratio of 100 percent means that a home sells each time one is listed.

The type of home you’re selling

The citywide average price and Toronto sales-to-new-listing ratio don’t necessarily reflect varying trends in different segments. Sometimes condo prices are rising at a time when house values are falling.

Location, location, location

Average Toronto home prices also mask hyper-local trends. TREB breaks down its monthly sales figures into specific areas, and this can be a good place to start. You’ll also want to zero in sales activity on your street or specific neighbourhood. What are your neighbours’ homes selling for? Also look at community amenities and access to public transit, as these are known to boost home values. Look up your address’ Walk Score, as many homebuyers, especially those looking for homes in a city, like this metric. It’s pretty much what it sounds like it is: an assessment of how walkable your area is (a high Walk Score means daily errands won’t require a car).

Your home’s specific features

Do you have a parking pad and/or a garage? In many Toronto neighbourhoods, parking comes at a premium. Similarly, finished basements and secondary suites have considerable appeal, especially in a pricey market like Toronto, where the potential to rent out part of a property can be a mortgage helper.

For condos, outdoor space and/or southern exposure are perks, as are low monthly maintenance fees. Storage space is a plus, especially in condos. Your building’s amenities can attract homebuyers, too. Buildings with family-friendly amenities, like playrooms or on-site parks, can help entice homebuyers who might otherwise have opted for a house with a yard, for instance.

Your home’s history

A heritage home appeals to some buyers but not to others who might not like being restricted in what can be done to the home’s exterior. As a result, they can be tougher to sell than a newer dwelling. Unsurprisingly, any connection to criminal activity or an investigation can erode home prices, too—former grow-ops, for example—while a unique past, like late novelist Ernest Hemingway’s former rental-apartment-turned-condo in midtown Toronto, can at least make the pending marketing process easier.

Other things to consider

Some say under-pricing your home in a hot housing market can spark a bidding war — there have even been instances of homeowners pricing their property at $1, just to see where the market takes it — but there is also research out of the US to suggest that a higher list prices lead to higher sale prices. A good realtor can provide valuable insight into how to price your home.

Related article: Inside Canada’s changing online listing landscape in 2019

9. Market your home

Before your home is on the market, you are going to need to have marketing materials created. Probably the most obvious example of this is professional photos because these are going to create the first impression of your home. Pictures from your smartphone won’t suffice. This is about creating a strong first impression of your home, after all, so leave it in the hands of an expert, not a shutterbug relative.

There is much more to marketing than pretty pictures and a flashy sign on a lawn. Justo offers a suite of options. For instance, Justo will craft a unique marketing plan, potentially including open houses, as well as a 3D virtual tour—so prospective buyers can virtually walk through your home from the comfort of their own. One great advantage to 3D tours is it can limit the wear-and-tear from busy open houses, reducing stress and extra work at an already-busy time.

Sometimes it’s worth it to think outside the box, especially for a unique property. One Toronto realtor even made a rap video to sell a “lil’ yellow house.” Movie-quality lifestyle videos have also been attempted to showcase properties, and drones have now become a part of some niche marketing efforts as well, providing breathtaking visuals that can show off a home in a unique way. Generally, the more eyes on your home the better, but it comes down to what you’re comfortable with.

10. Field the offers

Sooner or later, a well-presented home should be receiving offers, but there is more than one kind and the differences are important.

Firm versus conditional offers

There are firm offers, which have no conditions, and conditional offers, which do. In a buyer’s market, offers are more likely to come with conditions, whereas when demand is strong and there are multiple bids, many home shoppers simply want to win out.

A common one lets a homebuyer firm up their mortgage qualifications with a lender. Many homebuyers get a pre-approval, which means a bank has agreed to hold an interest rate for a certain period of time — though that doesn’t necessarily mean they’ll end up qualifying.

Sometimes buyers will make an offer that requires a home inspection to close. If you’ve already had your pre-list inspection, the likelihood of a nasty surprise decreases.

What to do if the buyer’s home inspection discovers a problem?

If you received a quality home inspection, there shouldn’t be any surprises here. Still, anything can happen, so you should have a plan in the event that closing home inspection identifies an unforeseen issue: namely, always try to compensate for the problem by reducing your price or giving a closing-cost credit.

The thinking here is simple. Why undertake the risk of a reno? They are disruptive, and budgets and timelines for projects can quickly spiral out of control, whereas offering compensation saves you from that kind of trouble. You know exactly what it’s going to cost you, and it’s easier to let the new owner’s fix whatever is wrong.

Are you offering any extras?

Then it comes to negotiating different matters like whether to include extras appliances, electronics, furniture, and more. Perhaps you’re moving to another country and can’t ship everything, or maybe certain items won’t fit your new home. (These extras can also be used as bargaining chips in the event that the buyer’s home inspection unearthed a problem.)

Chattels versus fixtures

To avoid any possible disputes, make sure you define chattels clearly in the purchase and sale agreement. Chattels are typically considered to be items that aren’t attached to the house; they wouldn’t require a tool to move. Think area rugs or curtains, a fridge or a toaster oven. If you like, you can add fixtures in the chattels section, but make sure there’s no confusion about what the buyer is getting. Spell it out.

Don’t be afraid to reject offers or counter-offer

You only get to sell this home once, so don’t settle for an offer you’ll regret later by short-changing yourself. A homebuyer’s first offer is very unlikely to represent how much they can actually afford to cough up (if it does, they are not getting good advice from their realtor).

You can cancel the counter-offer at any time before hearing back as well, so there’s really very little if anything to lose. There are not any legal obligations until the buying and selling parties have each signed on. Depending on how quickly you need to sell your home can dictate what your counter offer looks like. While offering below the list price may seal the deal, being firm can get you a better offer in the long run. You’ll also discourage low-ball offers this way.

If your offer is rejected, don’t sweat it. There are lots of reasons an offer might be struck down, and pricing is only one of them. A house hunter is likely looking at other properties, or their personal finances could have even quickly changed.

11. It’s closing time

The closing day is when the new owners take possession. Leading up to this, a few key steps need to be taken.

- Notify utility companies and other service providers, such as cable, Internet and landline, that you’ll be changing addresses

- Also, let the city know (you don’t want to keep paying property taxes!)

- Make sure your home insurance is set to cancel upon closing

- And if you’re moving out well before closing, tell your insurer when that is

- Hire movers if you haven’t done so already (Note: June 30th is the busiest moving day of the year in Canada, according to movers Two Men and a Truck)

- If you’ve purchased a condo, book the freight elevator well in advance, you won’t be allowed to use the regular lifts

Shortly before closing day, there will be more paperwork to sign with your lawyer. Once the new owner is on the title at one of the land registry offices, you receive your money, minus commissions, and related legal fees, of course.

12. Don’t lose that paperwork

Did you think you were done with the paperwork? It’s important to hold on to all documents relating to the sale of your home. You’re going to need them once tax season comes, and even after you file the Canada Revenue Agency could always call for an audit.

Speaking of the tax man, you must always report the sale of your home. The good news is if it was your primary residence, you won’t be paying any taxes on your capital gains. “In addition to reporting your principal residence on Schedule 3, you also have to complete Form T2091 (IND), Designation of a Property as a Principal Residence by an Individual (Other Than a Personal Trust,” according to the Government of Canada’s website. Your accountant will be able to answer any specific questions you might have.

13. Celebrate

Congratulations, you’ve sold a home—and hopefully for a tidy profit. Use a little bit of that cash to treat yourself, whether its dinner at your favourite local restaurant or a weekend trip to Prince Edward County. You’ve earned it.

Summary

Mountains of paperwork and a lengthy to-do list show that selling a home in Toronto is serious but ultimately rewarding work. The payoff isn’t hard to see. Toronto is a national economic driver, and about 100,000 newcomers arrive in the Greater Toronto Area each year, creating a strong demand for housing. Sellers are uniquely able to take advantage of these fundamentals that generally lift prices over time. And to be sure, the city has seen stratospheric price growth over the past decades, even after cooling periods are factored in. Indeed, if you do spend 20 years or so in your home, the chances of taking a loss upon resale diminish considerably. That said, very few people live in the same home for an entire lifetime, so it’s less a matter of if and more about when. Weigh all the pros and cons before deciding when the time is right for you for the best possible home-selling experience.

Related article: New Brokerage Splitting Listing Fees for Buyer and Seller Savings

- The Impact of Interest Rate Cuts on Toronto’s Housing Affordability - April 23, 2025

- Bank of Canada Holds Interest Rate Steady Amid Tariff Uncertainty - April 19, 2025

- The Impact of Interest Rate Cuts on Toronto’s Housing Affordability - April 11, 2025

{kind=link}